The Wall Chart and Other Financial Goals

Your monthly tabulation (from Steps 3 and 4) helps you see your savings rate – how much your income exceeds expenses each month. The amount of money you have saved, however, is not necessarily added to your bank accounts or investments. For example, you could be using that money to pay down your debts.

The purpose of Step 8 is to motivate you to keep making progress toward a point of financial ease. You can add lines to your wall chart to gauge and celebrate your progress toward additional financial goals. Or you may want to create a separate chart for tracking debt or other financial goals.

Case Study: Smith Family Decisions

As shown in the accompanying chart, Chris’ family spent some big money remodeling their vacation home into a year-round residence, but it decreased their average monthly expenses significantly, in addition to eliminating a second mortgage. Large one-time expenses still occurred – like braces for their oldest child in June of the second year – so it was important for Chris that a certain amount of money be set aside as savings for just such unusual expenses. After that “cushion” was set aside the priority became paying off the family’s large debt, and Chris charted their progress on a separate line (in black).

As you can see, Chris’ independence income line crossed above the expense line within the second year of following the program; however, with over $20,000 left in short-term debt (not even including mortgage debt), Chris did not feel “independent” yet – but she was on her way!

The purpose of Step 8 is to motivate you to keep making progress toward a point of financial ease. You can add lines to your wall chart to gauge and celebrate your progress toward additional financial goals. Or you may want to create a separate chart for tracking debt or other financial goals.

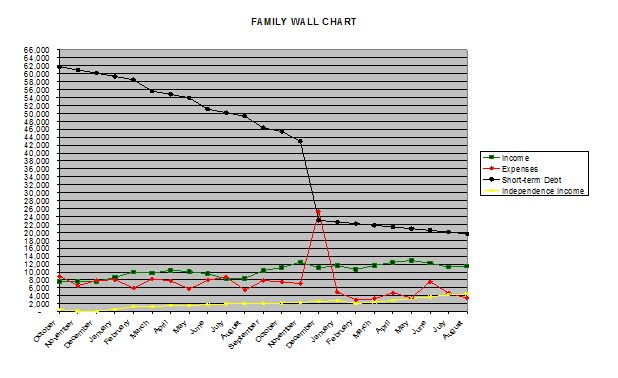

Case Study: Smith Family Decisions

As shown in the accompanying chart, Chris’ family spent some big money remodeling their vacation home into a year-round residence, but it decreased their average monthly expenses significantly, in addition to eliminating a second mortgage. Large one-time expenses still occurred – like braces for their oldest child in June of the second year – so it was important for Chris that a certain amount of money be set aside as savings for just such unusual expenses. After that “cushion” was set aside the priority became paying off the family’s large debt, and Chris charted their progress on a separate line (in black).

As you can see, Chris’ independence income line crossed above the expense line within the second year of following the program; however, with over $20,000 left in short-term debt (not even including mortgage debt), Chris did not feel “independent” yet – but she was on her way!