Step 8 - Investment Income

Capital is Money Invested to Create Income

An investment is placing your capital in some form of wealth other than cash with the expectation of deriving income. One approach is speculative investment: investing your capital in things like real estate, stocks or gold bars, with the hope that their value will rise and you can sell them later for a profit. The other approach is investing for fixed income – lending your capital to someone else and charging them a mutually agreed-upon interest rate for that use. This investment could range from a simple savings account to a bond.

Many people use bank accounts merely to store their savings for spending later, and they don’t pay much attention to earning interest. Capital, as opposed to savings, is amassed not to be spent but to be invested for a certain period of time. The whole point (for you, the investor) is what your capital earns over that period.

The income you receive from your invested capital is of a different nature than your job income. You receive it whether or not you go to work. So, on your monthly wall chart you will track that investment income separately from your other income – call it your Investment Income.

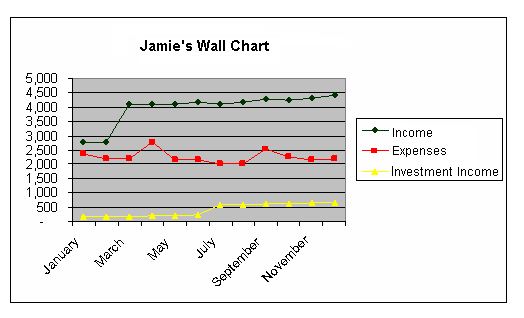

Case Study: Jamie’s Investment Income

At the age of 18 Jamie received a graduation gift from Uncle Joe in the form of a 20-year savings bond worth $20,000 and paying 6.75% interest. (Although this interest won’t be paid until year 20 when the bond “matures”, Jamie calculates the interest earned monthly). With that income, combined with the compounding interest from other investments, the yellow Independent Income line is slowly rising. Notice the jump in that line when Jamie put $15,000 from savings into a higher-yielding investment.

An investment is placing your capital in some form of wealth other than cash with the expectation of deriving income. One approach is speculative investment: investing your capital in things like real estate, stocks or gold bars, with the hope that their value will rise and you can sell them later for a profit. The other approach is investing for fixed income – lending your capital to someone else and charging them a mutually agreed-upon interest rate for that use. This investment could range from a simple savings account to a bond.

Many people use bank accounts merely to store their savings for spending later, and they don’t pay much attention to earning interest. Capital, as opposed to savings, is amassed not to be spent but to be invested for a certain period of time. The whole point (for you, the investor) is what your capital earns over that period.

The income you receive from your invested capital is of a different nature than your job income. You receive it whether or not you go to work. So, on your monthly wall chart you will track that investment income separately from your other income – call it your Investment Income.

Case Study: Jamie’s Investment Income

At the age of 18 Jamie received a graduation gift from Uncle Joe in the form of a 20-year savings bond worth $20,000 and paying 6.75% interest. (Although this interest won’t be paid until year 20 when the bond “matures”, Jamie calculates the interest earned monthly). With that income, combined with the compounding interest from other investments, the yellow Independent Income line is slowly rising. Notice the jump in that line when Jamie put $15,000 from savings into a higher-yielding investment.